While many believe insurance pricing is opaque and hidden behind complex models, the reality is quite different. Pricing actually leaks continuous signals. Every quote requested by a customer leaves behind breadcrumbs. This means it is possible to deduce how the premium shifts:

You can capture these patterns and reverse-engineer your competitors' pricing logic or the current market trends, and fine-tune your own insurance pricing strategy.

But the volume and velocity of quotes make it nearly impossible to manually decode pricing behaviors at scale. This is where Decision Intelligence (DI) comes in. With DI, you can automatically extract and structure these signals, transforming scattered quote-level noise into actionable intelligence.

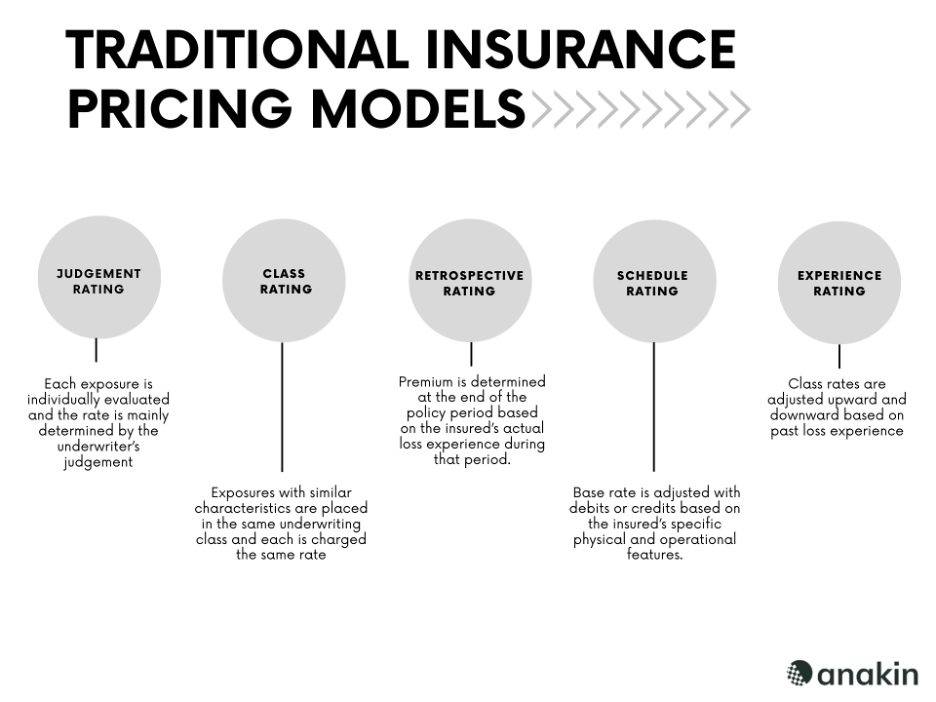

All traditional methods of pricing in insurance share a common flaw: they treat customers as broad, generalized "groups" rather than individuals. Instead of leveraging nuanced data, insurers often rely on rough approximations. The data used to build these groupings is also limited and imprecise enough to enable truly accurate risk assessment and pricing.

Such traditional approaches made sense decades ago. They simplified the creation and optimization of a multi-sector insurance pricing strategy to an extent. But in today's hypercompetitive world, they fall short as they struggle to capture future risk accurately. This often leads to overpricing for some insurers and underpricing for others. Ultimately, the market has a sense of unfairness that erodes trust.

DI in insurance Pricing is a strategic application of data and AI-driven insights to set and refine premiums in a way that optimizes profitability, balances risk, and delivers fair value to policyholders. Rather than relying solely on traditional actuarial methods, it integrates diverse inputs such as:

Decision Intelligence brings together techniques like predictive modeling, advanced actuarial analysis, and granular market segmentation to more accurately evaluate risk and anticipate future losses. What sets it apart is the continuous feedback loop: pricing strategies are not static, but dynamically monitored, tested, and adjusted as conditions evolve. This allows you to remain competitive, reduce pricing disparities, and ensure both financial stability and customer trust in an increasingly complex market.

Here are three reasons why DI is critical for building a successful insurance pricing strategy today:

Adopting DI in insurance pricing is not just about upgrading technology; it's about re-engineering the entire decision-making process. This transformation can be achieved through three foundational steps:

The first step in building a DI-driven pricing engine is establishing a strong and broad data foundation. Beyond internal datasets like policyholder behavior, claims history, and risk assessments, you must also capture macroeconomic indicators, telematics, and climate data.

But more importantly, you must track competitor pricing across a vast array of products: auto, health, travel, life, even niche covers like event insurance. This is because competitor moves in one product often influence customer choices and pricing dynamics across others. For example, if a competitor slashes life insurance premiums, they might balance it by tightening terms on health riders. This is something only visible with cross-product tracking.

Anakin supports this by scraping live insurance pricing at scale, across regions, demographics, and time horizons. For instance, when premiums shift after wildfires in California, you can quickly capture not just the repricing of auto and home insurers, but also competitive moves across travel and health categories.

Additionally, with insurance aggregators like Confused, PolicyBazaar, Insurify, etc. gaining prominence, you need visibility into how your products are positioned relative to competitors on these platforms. Anakin helps you go beyond surface-level pricing and capture key details such as insurer name, premium amount, policy duration, sum insured, and even claims history (where available) so that you can position your offerings competitively.

Ultimately, the goal of this step is to have a product-level view of the market, giving you the same transparency customers increasingly enjoy today.

Collecting data is only the beginning. The next step is turning it into insights that actually shape smarter premium decisions. Traditional pricing models typically rely on actuarial tables, historical claims, and statistical probabilities. Decision Intelligence overlays these models with real-world behavioral and competitive signals. This ensures premiums reflect both risk fundamentals and market context.

For example, if a competitor drops health premiums, DI can help uncover whether this stems from fewer hospitalization claims due to preventive care programs, or if it's simply a temporary acquisition strategy. By overlaying these insights with your traditional models, you don't just match competitor pricing, you make informed judgments about when to hold firm and when to reposition your value proposition.

This nuanced approach prevents reactive pricing and enables you to align premiums with true customer value and evolving risk factors, rather than just chasing competitors.

In the past, you could afford to revisit premiums and update your insurance pricing strategy on a quarterly or annual basis. But the rise of dynamic pricing in insurance has created markets where prices shift more frequently than that. Competitors can be seen constantly adjusting premiums based on demand, geography, and real-time risk data. Monitoring is all about actively watching these changes, identifying patterns, and understanding their implications for your own pricing strategy.

With DI-powered monitoring, every adjustment you or your competitors make feeds into a live feedback loop. This ensures that shifts in premiums, customer demand, or regulatory changes are detected in real time and analyzed to refine your models. The result is a pricing engine that stays responsive and competitive.

The future of insurance pricing lies in building adaptive, intelligent models that continuously evolve with changing market dynamics. Emerging technologies like blockchain promise greater transparency and trust in transactions. Similarly, IoT devices, from connected cars to smart wearables, will provide real-time data that makes risk assessment far more precise for setting prices and creating an effective insurance pricing strategy.

Combined with AI-driven Decision Intelligence, these innovations will move insurers away from static models toward intelligent pricing that benefits both providers and policyholders. The next frontier is not just about more accurate premiums. It's about creating a fairer, more responsive insurance ecosystem.

Written by Anakin Team